Where to Stash Your Cash

The silver lining of inflation and rising interest rates is that CDs and other accounts finally pay more than 0.000000001% interest. If you’re holding onto cash for an emergency fund or savings goal such as a house down payment, you may want to shop around for interest rates and know the environment before you commit your Benjamin’s.

Cash and Cash Equivalents

In the morass of technical financial terms, there are lots of definitions of cash. There are the notes in your wallet, the amounts in your bank accounts, and then a whole lot of other types of cash equivalents and near-equivalents. For this article, we’ll focus on accounts with explicit or implicit government backing and high, or at least predictable liquidity (you can get your money as fast as you expect to).

Why Have Cash Anyway

Some folks detest the idea of holding onto any cash, declaring “cash is trash!” because it doesn’t earn returns like other asset classes and inflation erodes its spending power. Others shout “cash is king” because it performs the key roles of currency: it’s a store of value, a unit of account, it’s a widely accepted medium of exchange, and it’s ready to go when you need it.

Let’s save the trash vs. king debate for another time and talk about reasons to hold cash.

Emergency fund. Nearly any other asset has high short-term volatility (stocks, crypto, real estate, bonds) or poor liquidity (bonds, real estate, alternative investments, etc.). Cash will probably have the same value tomorrow as it does today, and you can access it instantly or at least on a predictable timeline. Emergencies resist scheduling and cash is antidote to their untimely nature.

Near-term goals. Whether it’s the purchase of a home, car, or hole in the water to through money in (a.k.a. boat), you need return of your principal, not return on your principal. Recall that 87.5% of rolling 5-year periods in the stock market are neutral or better. Inside 5 years, your chances of losing money are too high to risk the purchase of a home, car, college tuition, etc. This is where cash is king!

“Bucket 1” in retirement. Retirees often want protection from market volatility. Holding several years’ worth of cash can allow longer-term “buckets” with stocks and bonds to recover from a decline without having to sell depressed assets in a down market.

When to Skip Cash

There are times when cash is about as appropriate landing long on a wet runway in a crosswind. It’s important to moderate rather than hoard cash for:

Retirement funding. If your life expectancy is over 5 years, and unless you’re well into your 90’s, it probably is, you need to outpace inflation with at least some of your money to fund your retirement.

Long-term goals. Inflation doesn’t need much foot-stomping right now. Stocks, bonds, and real estate are some asset classes that historically outpace inflation of periods of years. If you won’t buy a home, fund college, or sail around the world for 5+ years, holding cash is like leaving your gear down for the whole sortie. It’s important to take a bit more risk to get the returns you’ll need to fund your goals.

Types of Interest-Bearing Accounts

The paradox of choice can quickly become analysis paralysis when it comes to account options. Let’s take a look at what may be on the menu:

Bank Savings Account. Your current bank undoubtedly offers savings accounts that are meant to have few transactions per month. Other than your bank checking account this is usually one of the lowest interest rate accounts you’ll find.

Bank Checking Account. Your checking account may also offer a sub-atomic particle-sized amount of interest, but it’s probably not enough to help you build out the war chest you’ll need for future goal.

High Yield Savings Account (HYSA). The only real magic of a HYSA is that it pays a higher interest rate than what you may have as a traditional savings account at your bank. Many HYSAs are at online-only banks, so you add a +1 to the number of financial institutions on your roster with a HYSA.

Money Market Account (MMA). Your bank or investment brokerage firm likely also offers a money market account which acts like a hybrid between a checking and savings account. The interest rate is probably similar to a HYSA. Money Market Accounts do NOT carry FDIC insurance.

CD (Certificate of Deposit). Banks and Credit Unions issue CDs in variable amounts, interest rates, and maturities. I.e., you can buy a CD of any amount that matures in 1 month or many years and your interest rate will remain static. By offering you an unchanging rate, you can predict your earnings. By limiting your ability access the money until maturity, the bank knows how much money it can lend and for how long.

Brokered CDs. Many large investment firms (e.g., Schwab, Fidelity, Vanguard, etc.) sell Brokered CDs. They work very similar to bank CDs but can be sold prior to maturity without a penalty (but may have a transaction fee). They can also be called early by the granting institution if interest rates drop, so they have less of a guaranteed return. The rates on brokered CDs are generally better than bank CDs.

MYGA (Multi-Year Guaranteed Annuity). A MYGA is an annuity—an insurance product but probably not one that should set off your scam warning receiver. MYGAs function much like a CD, often with slightly better rates. Some MYGAs will allow partial withdrawals prior to maturity as well. The main problem with MYGAs is that you must be 59.5 years old to withdraw the funds without a 10% penalty tax on the earnings, so they’re not terribly appropriate for younger savers.

Treasury Bills. T-Bills are easily bought through www.treasurydirect.gov and have fixed maturities starting at 4 weeks through 52 weeks. They pay a fixed return during that period. If purchased through a brokerage, they can be traded prior to maturity if interest rates change, or funds are needed sooner. Earnings are taxed at the federal but not state level.

Savings Bonds (e.g., Series I Bonds). I-Bonds have had their heyday for the past two years as inflation has been high. They’re currently paying 4.3% and the rate will reset every November and May. Remember the main limits of I-Bonds: $10K purchase limit (plus LLCs and Trusts, plus $5K through a tax refund), 1-year minimum holding period (5 years without an interest penalty), and rates fluctuate twice a year.

Where to Find the Best Rates

The Internet has gotten awfully diffuse, so it can be quite difficult to sift through advertising and scams to find legitimate sources of financial information. Finding the best rates on cash products tends to be easy though.

Bankrate.com is a great search tool for both finding current rates and getting a sense of what banks you might need to do business with in order to get the best rates. Heads up that you’ll need to do some scrolling to get past the promoted banks which often pay lower interest rates.

Treasurydirect.gov is a painfully arcane site to log into, but otherwise it’s easy to learn about Treasury Bills and Bonds as well as purchase them. Compared to buying government bonds through a brokerage, this is an easily understood process.

Your Current Brokerage (e.g., Schwab, Vanguard, Fidelity, etc.) probably offers brokered CDs and a fairly simple process for purchasing them.

MaxMyInterest is a tool that will automatically move your money around to various institutions to get the best rates. It’s a paid service, but it does limit your workload. Competitor services are starting to come on line as well.

Many “robo” firms offer similar features to MaxMyInterest by continuously shuffling your dough to various banks offering higher rates..

Your current bank/credit union is a big easy button but may not pay the best rates. The convenience trade can still be worthwhile.

Boring Stuff (Taxes and Insurance)

The earnings from cash accounts have many names: interest, yield, dividends (credit unions), etc., but it all shows up on Schedule B of your tax return and it’s taxed at ordinary income rates. For most of you, this is 22% or 24%. When you earn a paltry 2-figure number of interest in a year, the tax bite isn’t much. But as interest rates climb, so will your tax bill.

Other than government bonds, states that have income taxes will tax the returns from your cash accounts.

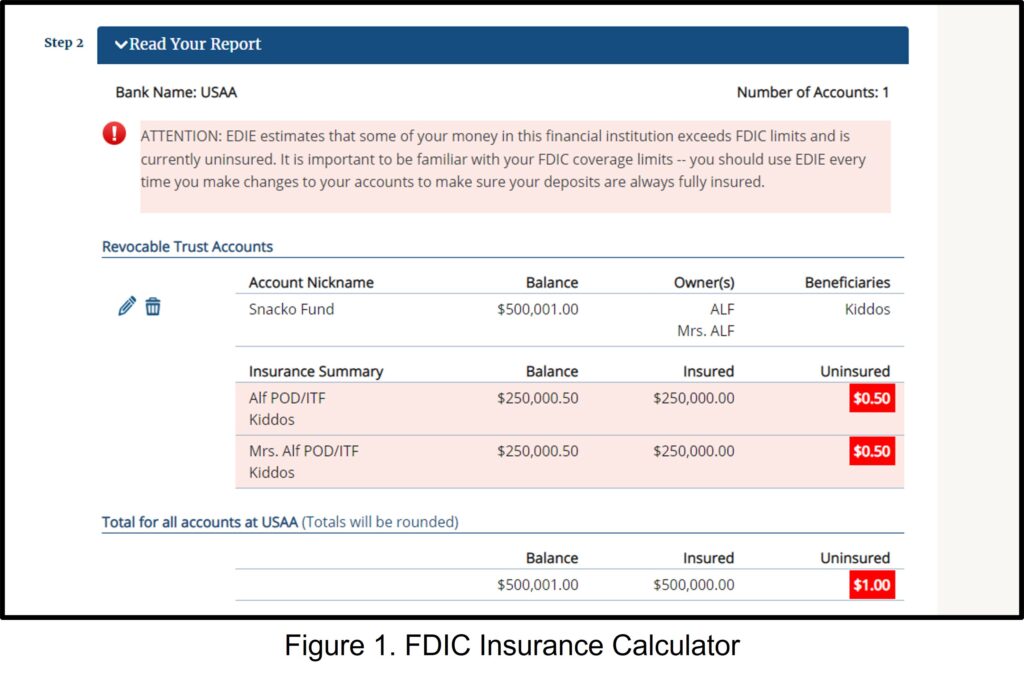

During the 2008-2009 financial crisis, hundreds of banks failed, but it was an orderly decay of those institutions as government regulators facilitated their purchase by other healthier banks. The Federal Deposit Insurance Corporation (FDIC) insures cash accounts in banks for up to $250K per account owner. Figure 1 below shows the output of the FDIC’s insurance estimator. If you’re not sure whether your account is fully insured, you can verify it with this tool.

Credit unions also offer $250K per depositor insurance through the NCUA (National Credit Union Administration) and it’s functionally identical to FDIC insurance. NCUA also offers a tool to validate the amount of insurance you have.

If you’re nowhere near $250K in a single institution, then as long as it’s an FDIC/NCUA covered institution, you’re in good shape. If you’re close to the limit, then current rates might push you over and you’ll need to consider spreading your eggs to other baskets to be fully insured. Beware of bank lookalikes that are not FDIC insured!

Cleared to Rejoin

Cash generally isn’t sexy, but there are years when it’s the best performing asset class. Undoubtedly, you’ll need some even if you don’t like to hold onto lots, so it’s worth paying attention to the types of cash accounts and tradeoffs with each. Action steps you can take today with your cash:

- Determine how much you need for an emergency fund and near-term goals.

- Determine how long you’ll need to hold each chunk of cash.

- Research the best rates for the account types you’re comfortable using.

- Consider opening a small trial account with a new type (e.g., brokered CD or Treasury Bill) to expand your repertoire of useful cash tools.

Fight’s On!

Winged Wealth Management and Financial Planning LLC (WWMFP) is a registered investment advisor offering advisory services in the State of Florida and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Winged Wealth Management and Financial Planning (referred to as “WWMFP”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute WWMFP’s judgement as of the date of this communication and are subject to change without notice. WWMFP does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall WWMFP be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if WWMFP or a WWMFP authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.