Kid-Span and the Spans

Frequent victims of my blogging know I’m a stark-raving fan of Die With Zero by Bill Perkins, so I’ll promise this isn’t a blog about a band called Kid-Span. Perkins’ message that we should seek maximum life fulfillment rather than maximum dollars by maximizing the years that we have health, energy, and some money rather than just accumulating greenbacks until we can’t realistically spend them on things we enjoy resonates with me so much that it’s become the core of both my financial planning and my own journey of life optimization.

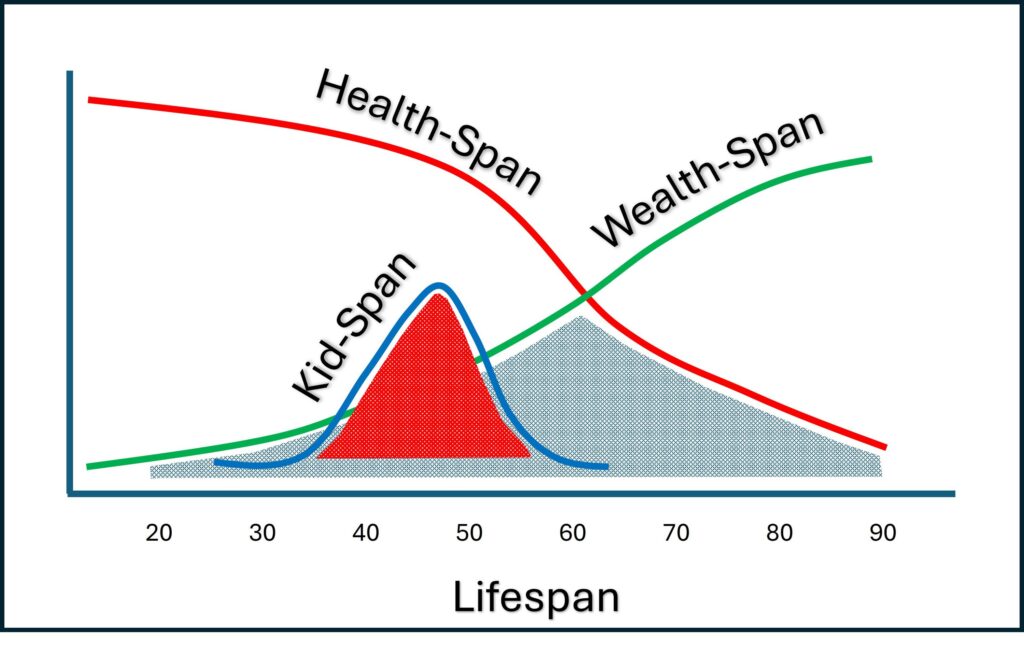

There’s a concept that Die With Zero hits on, but I think needs more attention: the “Spans.” You have a Lifespan—a number of laps around the sun. You have a Health-span—a declining number of adult years that you can engage in active pursuits. You have a Wealth-span—a (hopefully) increasing net worth through your adult years. And you also have a Kid-Span—a parabolic number of years to enjoy your kids. Let’s talk about your Spans.

Lifespan

We get a vote on maximizing our lifespan with healthy eating, exercise, stress management, safe choices, etc. But fate gets a veto. As a 21st Century American, if you make it to your 60s, you’ve got a great chance of living well into your 80s. Unfortunately, a long life without health, wealth enough for dignity, and enjoyment of relationships may not be your most fulfilling lifespan.

Health-span

I’m on my 50th lap this year, and I’m on a bit of a jihad to finish this one in better shape than my 30th. While I can train for more pull-ups, the brutal reality is I recover slower, metabolize slower, run slower, sleep poorer, and give up muscle mass faster. I nudge my health, but I can’t reverse the clock. In the next two to two-and-a-half decades, I’ll lose my ability to engage in many of the active pursuits I truly love today. It’s go time for skiing, mountain biking, and endurance events. This is my health span. Youth may be wasted on the young, but I’m not giving up my health without a fight.

Wealth-span

Military and civilian earnings and wealth accumulation follow a similar trajectory. At the fight’s on, we adult with modest income and almost no wealth. We usually hit peak income in our late 50’s through retirement in our 60’s.

Peak wealth often occurs in the years before we die because compounding runs away like an auto-accelerating GE motor. This phenomenon is worse for those with beach-worthy six-pack abs as savings muscles and tiny, T-Rex, atrophied little spending muscles. Peak wealth late in life is a recipe for dying with a big pile of dollars and a small pile of memories.

The problem with our Wealth-span is knowing, “When do I have enough?” Perkins offers a reasonable way to think through this, and of course, I’m a fan of financial planning and software tools to nail down answers which colors my approach. Ultimately, like all financial planning questions, there’s a math answer and a “sleep at night” answer. “Enough” will be about contentment, thoughtful planning, and a reasonable number of dollars.

If our health is good, Wealth-span is the worry-generator. If we spend too much too soon, we’ll eat cat food in retirement. If we save it all until the end, we’ll miss out on memory-making…during the Kid-span.

Kid-span

As infants, our kids don’t care about trips to feed Benjamins to the mouse. They don’t care what clothes we doll them up in. We care about the time we get with them and the experiences we share as they progress from toddler to Pre-K to elementary school, and at some point, they start to care about time and experiences together too.

As we approach high school, we may lose access to our kids. The high school calendar matters when the middle school calendar didn’t. Grades and academic achievement start to matter. Social and extracurricular activities begin to demand more of their time. The time available for cool trips, bonding over shared interests, and just enjoying calendar whitespace dries up as nonstop busyness forces calendar Tetris for every family member.

As our kids launch to college and adult lives, the Kid-span ends. We might have time for them, but they have their own lives. The overlap can dry up. It’s not all doom and gloom. It’s just the normal course of things and it creates an imperative: pick your verb–but you may want to align/optimize/maximize your Spans with the Kid-Span as it may be the shorted Span.

Optimizing Your Spans

Die With Zero suggests that the blue-shaded area of the Span chart above is the alignment of your Health-span and Wealth-span. You have the money to do the things you’re fit enough to do. The red-shaded area represents when you have the greatest access to your kids, some amount of wealth, and hopefully a solid dose of health.

The red-shaded region implies insufficient wealth for maximizing the Kid-span because income hasn’t peaked and compounding needs more time. There’s a wealth gap that could prevent maximizing the Kid-span.

Setting aside the obvious that this may not be a surmountable problem, how can we address the Kid-span wealth gap?

- Save early and late. For many families, surging on TSP/401(k)/IRA before peak child experiential years then reducing retirement savings to boost memory-making expenditures during the Kid-span followed by maximizing saving after the Kid-span is a great way to harness the power of compounding.

- Think about it this way—if you’re already at or above glidepath for your retirement needs, will spending $10K more on vacations for 10 years instead of investing $10K more in the TSP knock you off course? We can math that out, but for diligent savers it probably won’t.

- Prioritize Roth IRA and taxable accounts. This isn’t a blanket good idea, but dollars in Roth IRAs and taxable accounts are very accessible during the Kid-span. If you surge into those accounts in your early working years, you won’t be staring at a pile of “post 59 ½” dollars you can’t spend on a cruise with the mouse.

- In retirement, go where the money is: work. Few of us want to age in place at our workplace, but stepping out of the workforce early isn’t inherently virtuous either. What if the bill-payer for the Kid-Span is working a few extra years?

- Hit up the Geezers. One of the most profound statistics from Die With Zero is that the average age for receiving an inheritance is about 60. Our financial stories are etched in stone at 60. Asking Scrooge and Mrs. McDuck for early inheritance isn’t going to work in every family, but Die With Zero makes a great stocking stuffer if you want to start planting seeds. Maybe just invite them to the memory making event as a starter…

- Get your math on. Consumer-facing financial planning software is getting better, but spending a few (thousand) pesos with a financial planner to see what your wealth trajectory looks like may deliver peace of mind that you don’t have to keep maximizing retirement savings every year during the Kid-span.

- Prioritize. It’s probably going to be a brutal few years in the housing market. The days of cheap mortgages to buy reasonably priced McMansions may be in the rearview mirror for now. Can you tolerate less house to have a better Kid-span?

- Discipline your dollars. Few families know their average monthly or annual spending with any accuracy. Life is busy, budgeting sucks, credit cards are easy… there’s a ton of reasons why. If we don’t tell our money where to go, we’ll wonder where it went. Being relentlessly frugal on the things we don’t value can provide for more lavish spending where it counts in the Kid-span.

Cleared to Rejoin

If you’re still reading, you have kids. They drive us a little crazy, but they are the biological imperative. They are the center of our gravity. We only get a short Kid-span with them. Die With Zero is a great start, but when was the last time you thought about your Lifespan alongside your Wealth-span, Health-span, and Kid-span? When can you use the time, wealth, and health the best for your family?