Part 3: The Why and How of Lieutenant Millionaires

With great power, comes great responsibility. Spiderman’s uncle Ben usually gets credit for this axiom, but the Supreme Court has used it too, giving it a little extra throw-weight in my book. Lieutenants, like all military officers, are endowed with the power to lead and potentially end the lives both the enemy and the women and men in their charge. There is no greater power.

Born of this power is the responsibility to wield it in good fashion. When it comes to the increasingly handsome and secure compensation package you receive, that responsibility implies an irreproachable level of stewardship. Your implied authority grows when you are clearly not living beyond your means.

It grows even further when you’re the squadron’s authority on the benefits of investing early and often. It follows that you have the power to build wealth for your future, therefore you have the responsibility to do so.

What you choose to do with your future wealth matters little when you’re starting to build it, but I’m willing to bet that in the course of becoming a superior officer over the years, you’ll nurture the character necessary to put your future wealth to admirable use for your family and the causes that inspire you.

You get no such choices if you don’t use the Time Value of Money to build wealth in the first place. Since you’re reading this third installment, I’m going to assume you’ve already bought into that.

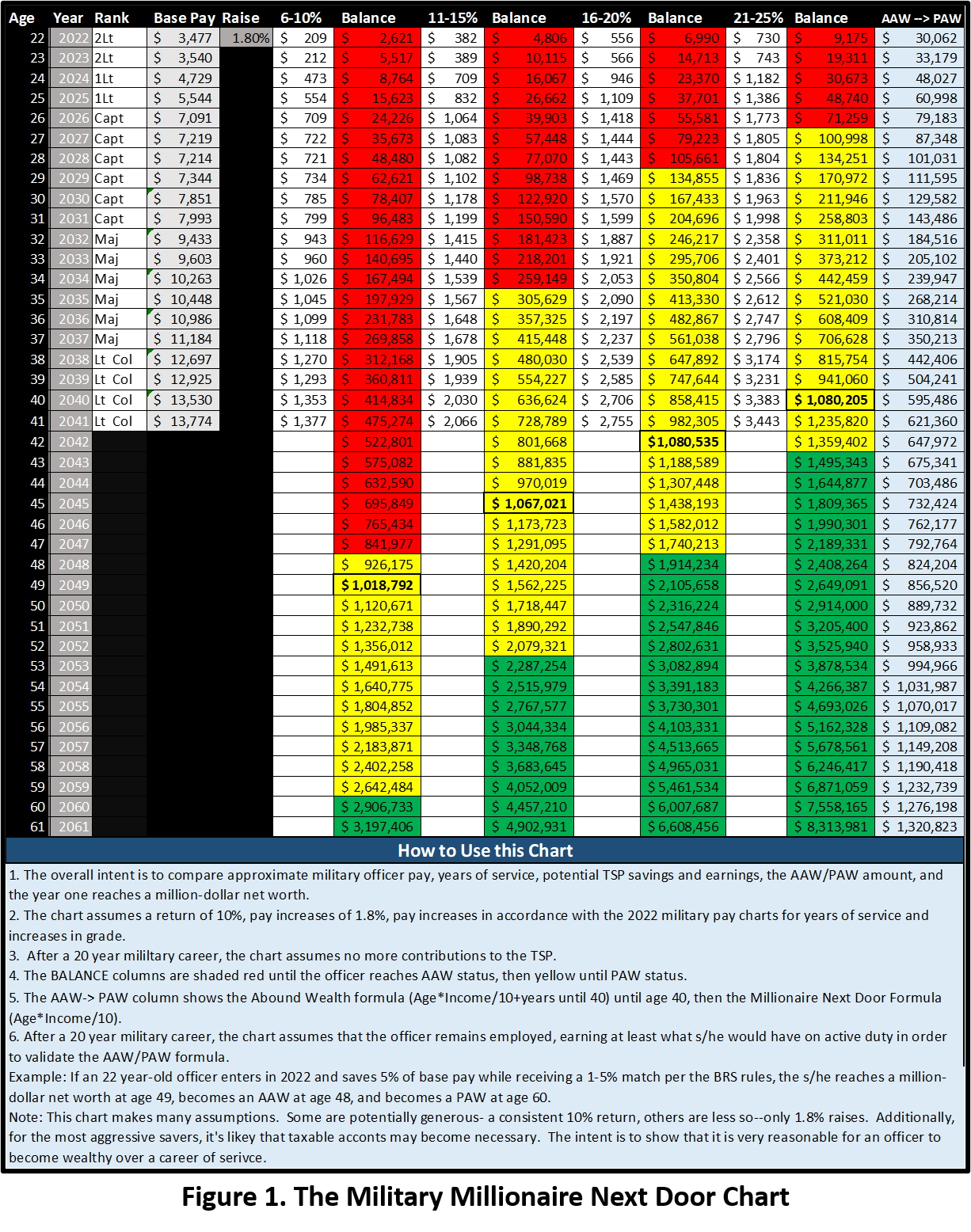

In the Five Pillars of Investing, we looked at the importance of considering investment location, allocation, costs, taxes, and behavior. Let’s take a look at how these can make you a (multi-) millionaire, starting with Figure 1. This chart has the following assumptions:

- Start as a 22-year-old 2Lt (2019 pay scale)

- Invest in the TSP 5%, 10%, 15%, or as much as 20% of your base pay

- Invest ONLY for a 20-year career, then never again

- Assume a compound rate of return of 10%

We’ll dissect the assumptions in a moment, but let’s take a look at how long it might take to achieve millionaire status at each rate of investment:

- 5% – Age 49, 27 years

- 10% – Age 45, 23 years

- 15% – Age 42, 20 years

- 20% – Age 40, 18 years (still on active duty!)

Worst case, you are likely to achieve a seven-figure net worth in your 50’s, using only the TSP and significantly under-saving as a percentage of your income. So, you’re sayin’ there’s a chance…

When you Assume…

Figure 1 implies that with the TSP alone, Lieutenants should expect to become millionaires. I do believe that, but market returns are both critical and unknowable. My crystal ball is permanently Code 3, so I can only rely on the past performance of the market, which I’m obligated to remind you, is not a guarantee of future returns. Okay, disclaimer aside, here’s some more thoughts on the assumptions in the chart, plus the bonus explanation of the color scheme:

- Time in grade progresses in a “In the Promotion Zone” timeline. That could change, but your monthly savings habit shouldn’t.

- Pay increases with time in grade are in line with historical increases.

- A flat 1.8% COLA on basic pay. That number will fluctuate over the years.

- The Blended Retirement System will continue to match 1% for the first two years, then up to 5% after that.

- The investor leaves the money in the TSP (or rolls it to an IRA) after military retirement and does not consume it.

- In the later years, it’s possible that an investor might be putting away more than the annual TSP limit (currently $20,500). As long as the investor still puts that money into a similarly performing portfolio outside the TSP, (preferably in an IRA) then the climb profile is not affected, only the tax considerations.

What’s with the Color Scheme?

Lieutenants who intend to be millionaires would do well to read (or listen to) The Millionaire Next Door: The Surprising Secrets of America’s Wealthy, by Dr. Thomas J. Stanley. A key observation from this study is the climb profile of millionaires’ wealth. Dr. Stanley noted that “average accumulators of wealth” had a net worth (assets minus liabilities) equivalent to:

Age x Income ÷ 10 = Net Worth

For example, if your income is $100K, and you’re 40, you should have a net worth of $400,000. This doesn’t have to be all in the TSP, but the bulk of it will be for many officers. But, if you’re a 24-year-old O-2 and just staring out this formula requires you to have:

24 x $72,000 ÷10 = $172,800!!!

You’re forgiven if you cry B.S. to that. Dr. Stanley’s formula desperately needs compounding time. A common modification to the formula for those under age 40:

Age x Income (10 + # Years until age 40)

24 x $72,000 ÷ (10 + 16) = $66,461

We’ll come back to this figure in a minute, but let’s talk about the colors in Figure 1. Dr. Stanley found that average accumulators of wealth (AAW) had net worth according to the formula above. But a subset of those who were truly diligent savers were “prodigious accumulators of wealth” (PAW) and had a net worth two times that of the AAWs. (Spoiler alert, it’s probably not helpful to suggest a formula for becoming a PAW prior to one’s forties, so no extra formulas for that.)

The light blue column in Figure 1 is labeled “AAW->PAW” and it uses the modified formula up to age 40 then the Stanley formula, based on projected income to suggest what an AAW should have accumulated. (The AAW numbers assume that the investor continues to work after military retirement, earning a salary that continues to grow at 1.8%.)

In each “Balance” column, the red shaded cells indicate that the investor has not reached AAW status yet. When the cells turn yellow, the investor is an AAW, but not yet a PAW. The green cells indicate that the investor is now a PAW.

Why do I Care about AAWs and PAWs?

If you aim at nothing, you can hit it consistently, but that’s no way to prepare for your retirement years. This series on Lieutenant Millionaires has not once mentioned credit score, the ear-worm-generating jingle and red herring number that our consumption-driven society seems to focus on. Credit score is not a measure of anything but one’s use of debt.

Far too many people have a high credit score and paltry net worth. Since one cannot borrow to finance retirement (lenders like you to have a job), net worth is the number to pay attention to. As I stated earlier, I do not recommend building wealth so you can Scrooge McDuck through your piles of gold. Rather, build wealth so you have choices in life like retiring without having to move into your kids’ basement or perhaps taking your whole family on a cruise or donating to your favorite cause.

You cannot donate a credit score. You can live off of your net worth. Even if you do not desire to become an AAW or PAW, I recommend “stepping on the scale” and tracking your net worth annually. It’s an easy and productive reality check.

If this AAW and PAW concept resonates with you, you might be a bit frustrated in the early years. Stay the course. Our math suggested that a 24-year-old O-2 should have nearly $72,000 in net worth (remember that’s cars, homes, investments, etc.) but Figure 1 suggests that even saving 20% and getting a 5% match means that you’re 27 before you become an AAW.

Congratulations! You’re not even 30 and your net worth is gusting towards $100K? I promise you that if you’re even trending towards AAW status in your 20’s, you’re breathing rare air among your fellow officers. Stay the course.

Cleared to Rejoin

With great power… You have an outstanding income and compensation package that only gets better. An officer leads by example with fitness, duty performance, and leadership in all aspects of readiness. Your finances are not exempt. If you’re going to be excellent in all you do, add retirement investing to your list. You will not regret it as you build options for your family and set a remarkable example for those you lead.

Fight’s On!

Winged Wealth Management and Financial Planning LLC (WWMFP) is a registered investment advisor offering advisory services in the State of Florida and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Winged Wealth Management and Financial Planning (referred to as “WWMFP”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute WWMFP’s judgement as of the date of this communication and are subject to change without notice. WWMFP does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall WWMFP be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if WWMFP or a WWMFP authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.